Many business owners ask, “Do I need to recalculate my estimated taxes during the year, or can I just use the payment coupons from last year’s return?”

If your income changes during the year, your estimated tax payments should change too.

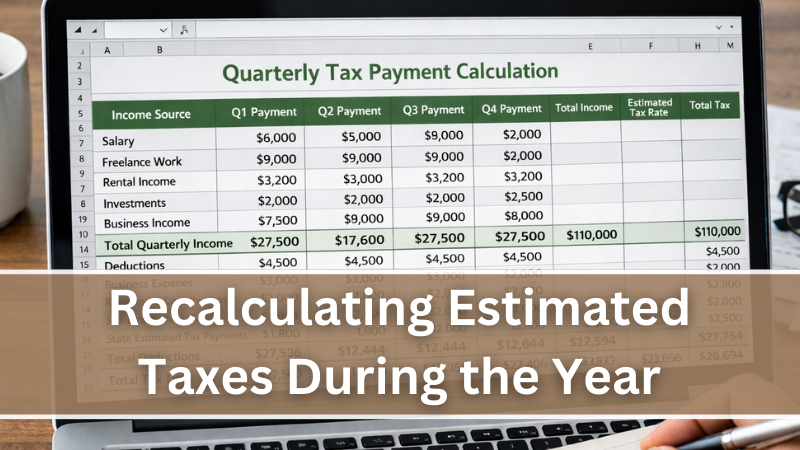

Estimated taxes are intended to track your current-year income. But in practice, many small business owners rely on prior-year numbers because they are convenient and feel safe. That approach can work if revenue, margins, and owner distributions remain steady. It becomes risky when a business experiences growth, improved profitability, or an unexpected transaction.

A common follow-up question we hear is, “Why did my small business owe so much in taxes this year even though I made quarterly payments?” In most cases, the quarterly payments were based on outdated information. The business grew, margins improved, or compensation increased — but the estimates stayed flat. The difference accumulates quietly throughout the year and shows up in April.

Taxes follow profit. If your books are not current, your tax estimate is guesswork. If bookkeeping is delayed by even a month or two, you cannot accurately evaluate year-to-date income before each estimated tax deadline. That makes proactive tax planning nearly impossible.

There is also confusion around safe harbor rules. Safe harbor can help you avoid underpayment penalties, but it does not guarantee that you will not owe a significant balance when you file your return. Avoiding penalties and managing cash strategically are two very different objectives.

Businesses that avoid surprise tax bills do something simple but disciplined. They close their books monthly. Before each quarterly estimated tax due date, they review year-to-date income and expenses. They recalculate projected federal and state tax liability based on actual performance. If income has increased, payments increase. If income softens, payments can be adjusted accordingly.

This process is not tax preparation, but it can be aided by ongoing tax advisory.

If you are unsure whether your estimated payments reflect current-year performance or last year’s assumptions, it may be time for a recalculation before the next deadline. Quarterly adjustments are often the difference between a manageable payment and an unpleasant surprise.

If you’re tired of surprise tax bills, let’s talk. We have full service tax, advisory, and accounting services for your small business needs. Contact us at help@sbsaccountants.com or 770-745-4283.